October 2022 Market Review

By Clint EdgingtonPosted on November 1st, 2022

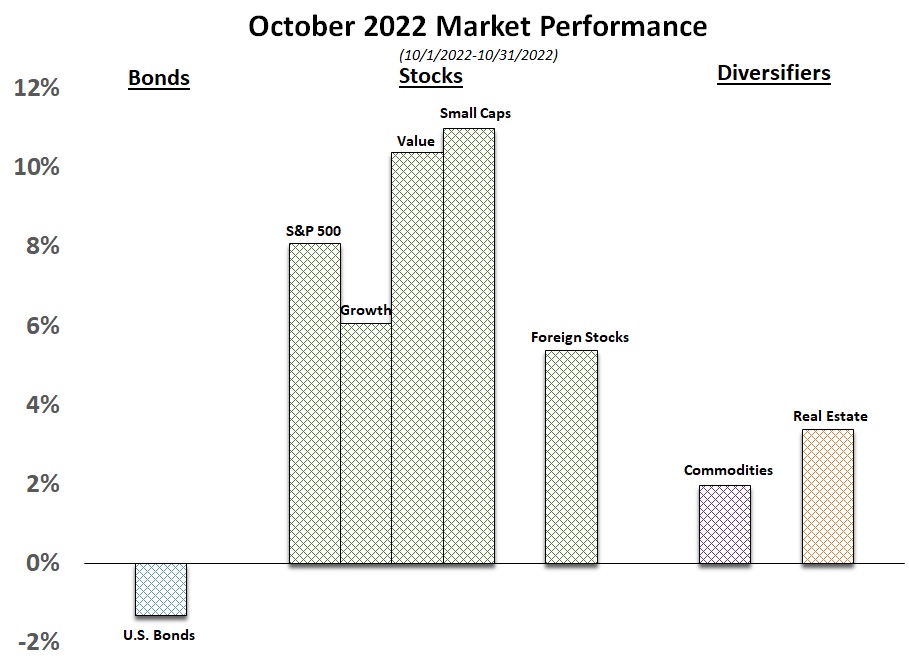

After a rough September, markets rebounded in October with the first monthly gain since July. After two quarters of contracting, GPD growth came in higher than expected at 2.6% for the third quarter. Investors were encouraged by the data, and most sectors posted notable gains. Value continued its outperformance against growth with the new backdrop of higher interest rates having to finance less cash flow centric businesses. Bond prices were pushed down, however, with interest rates continuing to rise in October.

Inflation data released in mid-October showed inflation slowing slightly from 8.3% in August to 8.2% in September. However, core inflation increased 0.6 percent in September; increasing 6.6% over the last 12 months. The next Federal Open Market Committee meeting, scheduled this week, will likely see another 75-basis point interest rate increase based on the latest inflation data. The Committee will meet again on December 14 for the set final rate increase of the year, and the market is roughly split in the thoughts as to whether it will continue with the projected .75% increases or something less than that. While inflation appears stubborn, the Fed’s previous increases have dramatically increased loan costs and have significantly slowed the real estate markets.