Q1 2026 Market Review

By Clint EdgingtonPosted on April 20th, 2026

My 15-year-old son is currently taking a beginner macroeconomics class in high school, and it has led to some enjoyable discussions at home about markets and current events. This past quarter offered a good opportunity for him, and seemingly for us, to determine the themes impacting the financial markets.

In many ways, the drivers of market performance felt relatively straightforward.

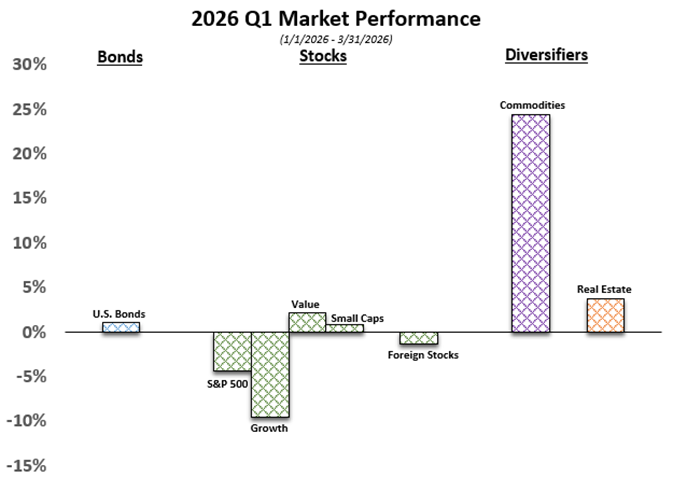

Why did commodities spike almost 30%? He nailed it, “If there’s less oil and demand doesn’t go down, prices go up.”

Equities down? Easy, “War likely impacted economic growth and the money companies will make.”

Value outperforming growth? We discussed how oil companies, with potentially higher revenue, would be represented in the Value indices and he understood the divergence.

These explanations and largely correct. However, as is often the case in markets, the full picture is more nuanced and frankly I’m not entirely sure of some of the cause and effects.

The Impact of Geopolitical Events

The Iran war, which abruptly began on February 28, clearly impacted markets and will hold the attention of investors for the near term. When, and if, this conflict reaches a resolution (recognizing that geopolitical events rarely conclude cleanly), we can expect a good chunk of these trends to reverse.

Prior to this, the dominant theme driving markets was interest rate expectations. The question is, once this war closes out will we return to that framework?

Value vs. Growth

One of the more interesting developments this quarter wasn’t just the outperformance of value stocks relative to growth. At first glance, this appears consistent with both the old and new theme:

- higher interest rates (which tend to weigh more heavily on growth stocks)

- rising energy prices (supporting value sectors), and

However, a closer look reveals a more complex story.

Notably, nearly half of the value outperformance occurred before the onset of the Iran conflict. This suggests that the divergence cannot be fully explained by energy prices or geopolitical developments.

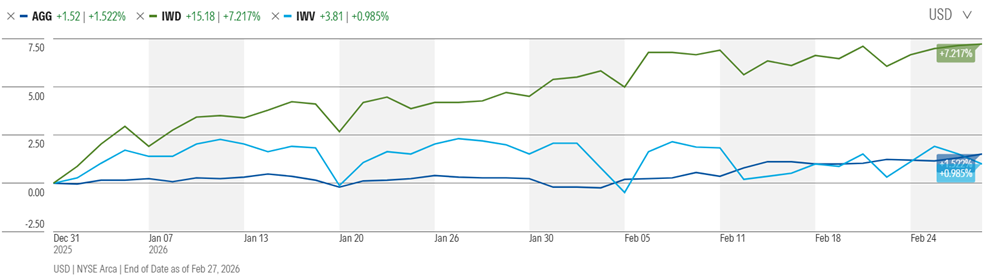

A natural explanation would be the continuation of the “higher for longer” interest rate narrative. Typically, in such an environment bond prices fall (yields rise), and growth stocks underperform due to the higher discount rate applied to future earnings.

Yet during much of this pre-conflict period, bond markets remained relatively stable, indicating that expectations for higher rates were not materially increasing.

So, what explains the move? There is no single clear answer, but several factors likely contributed. Investors with positions in the previously red-hot tech and AI markets were likely overweight in those positions. Watching them slowly go down and, not wanting to incur taxes in 2025, held off until the new tax year to reduce their positions, which could explain the divergence occurring in January.

A New Theme or Just Temporary?

Should we think of this as a new theme, or just an aberration? Likely in the short-term rotational dynamics and positioning will continue to support value over growth. We may see the impacts of that in the fourth quarter of this year; but I do not believe it will become a long-term theme.