Q2 2025 Market Review

By Clint EdgingtonPosted on July 7th, 2025

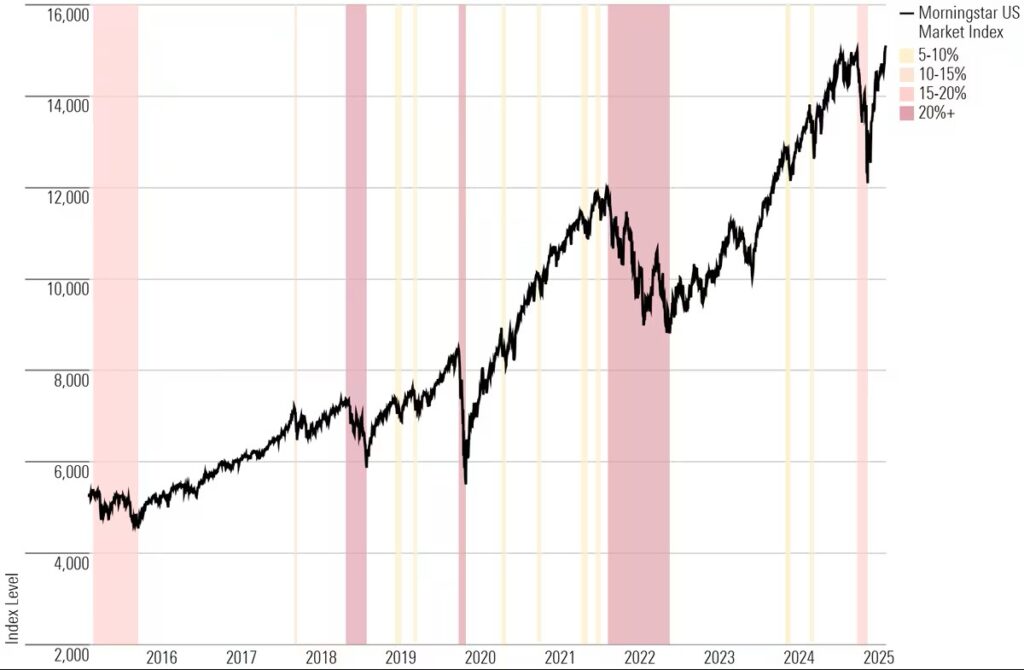

The quarter began with equity markets continuing and deepening the previous quarter’s slump to a free fall due to Trump announcing broad tariffs and the potential of a global trade war. From mid-February to April 8, 2025, the S&P 500 dropped 19%, almost entering “correction” territory. Steady hands prevailed, however, and fears receded when Trump offered a 90-day delay to allow for negotiations. The markets reversed to bring forth equity markets’ best quarter since 2023.

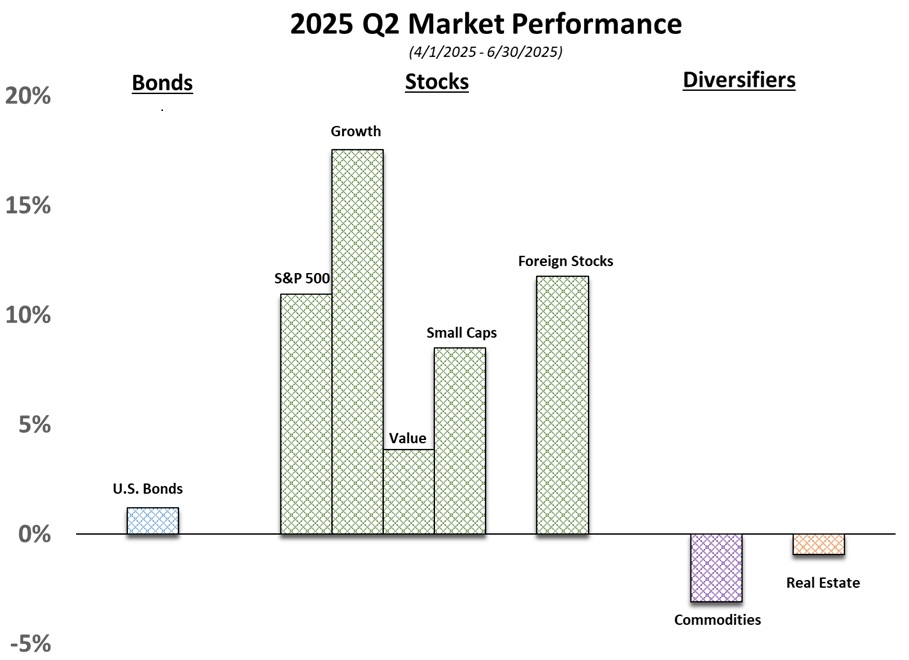

Q1 earnings’ results were generally positive, and macro fundamentals remained robust. International markets lead the way with 12% growth, and the U.S. close behind at 11%. Growth reversed Q1’s trend and trounced value, with the Magnificent 7 (as discussed previously) leading the way.

Fixed income markets slid in the beginning of the quarter due to the same tariff fears, and the potential inflation that could arise. Over the quarter, however, fixed income gave small positive returns as the yield curve shifted down slightly; more with shorter term fixed income, as belief has set hold that rate increases are in the rearview mirror and that there’s the potential for a slight rate cut in September.

Looking at the quarter ahead

Trump’s “One Big Beautiful Bill Act” focused on extending his 2017 tax cuts seems largely priced into the market, with its passage not impacting markets. The 90-day delay on tariffs is becoming the focus at the time of this writing again but likely will be delayed again or have different outcomes for different countries in various phases of negotiation.