Maximize Your Tax Savings by Utilizing a Health Savings Account

By Anne ZavagliaPosted on July 12th, 2024

Health savings accounts (HSAs) are available to those who participate in a high-deductible health plan. HSAs are tax-advantaged accounts that offer tax savings now and can be used as a tax-efficient vehicle for retirement.

HSAs combine the best of both worlds from qualified retirement plans such as 401ks, traditional IRAs, and Roth IRAs. Contributions to an HSA are excluded from taxable income, the way pre-tax contributions to a 401k or IRA are. Like Roth accounts, the contributions then grow tax-free and there are no required minimum distributions later in life. Withdrawals are tax-free if used for qualified medical expenses.

The maximum contribution for individuals in 2024 is $4,150 and $8,300 for a family. A $1,000 catch-up contribution is allowed for those 55 and older. Contributions to an HSA can continue while working up to six months before Medicare eligibility (age 64.5). Withdrawals for any reason are allowed after age 65 without a penalty, and withdrawals for medical expenses are always tax-free. Withdrawals before age 65 for non-medical expenses are subject to a tax and a 20% penalty.

The money in an HSA can be invested the same way one would with an IRA or 401k. Often people do not take advantage of this and leave their money sitting in cash. Because the investments grow tax-free, rather than treat the account as a savings account for current health spending, it can be used as an investment account. Withdrawals for qualified medical expenses are tax-free now and in the future.

If you can afford it, paying for medical costs out of an emergency fund or regular savings offers the opportunity to allow money in the HSA to grow. In addition, there is no time limit for when a medical expense can be reimbursed. Receipts and invoices with the expense details must be saved for the reimbursement.

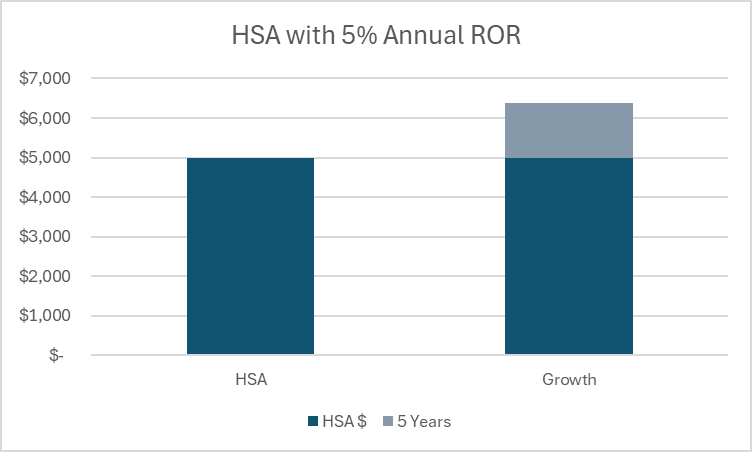

For example, a 5,000 dollar procedure paid out of pocket this year, can be reimbursed 5 years from now from the HSA account. In the meantime, the $5k in the HSA, assuming a 5% annual return, will have grown to $6,380. Furthermore, the $5k was funded with money excluded from taxable income. Someone in the 22% marginal tax bracket saved $1,100 in taxes and grew their HSA account by $1,380.

Medical expenses are often high later in life. This is where HSA accounts become an important part of your retirement plan. It is estimated that 70% of people over age 65 will need long-term care at some point. HSA accounts can be used to pay for long-term care itself, or long-term care insurance premiums. Medicare expenses such as Medicare Part B, Part D and copays. Rather than pull a 100% taxable distribution from an IRA during retirement for medical costs, an HSA can be used instead.

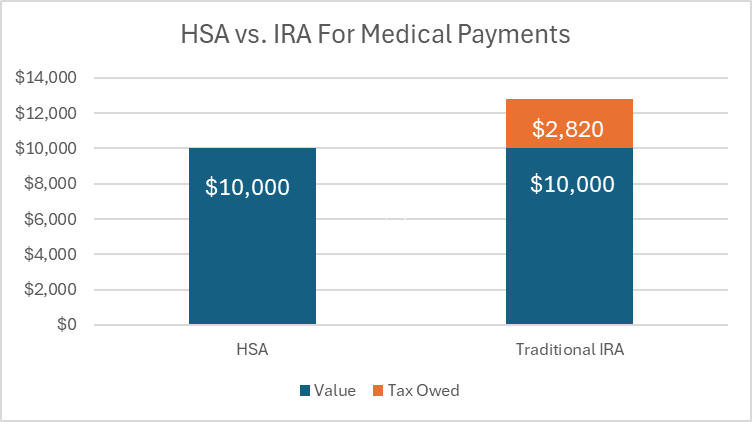

Thinking about the growth of $5,000 again. Over 20 years and with a 5% annual return, it will grow to $13,266. A $10k medical expense paid at age 70 from the HSA account wouldn’t be taxed. If pulled from an IRA to pay the same expense it would be included in taxable income. Someone in the 22% marginal bracket would need to take an IRA distribution of $12,820 and owe $2,820 in taxes to pay for the same expense.

Utilizing HSAs for health care during retirement allows other retirement savings accounts to continue growing to be used for living expenses, travel and other goals.

If your HSA account passes on to your spouse at death, they can treat the HSA account as their own and continue receiving the same tax advantages. The account becomes taxable to non-spouse account beneficiaries in the year of your death. Unlike IRAs, they must take it in a lump sum vs over 10 years.

Consider optimizing expenses being paid from the HSA account to ensure its use during your lifetime, vs using non-HSA accounts for medical expenses. This will allow non-HSA assets to pass to non-spouse beneficiaries in a more tax-favored way.

Ultimately, an HSA account allows you to have an account earmarked for health care, the same way you would for retirement or college, with triple tax savings.