Proposed Tax Legislation

By Anne ZavagliaPosted on September 29th, 2021

The House Ways and Means Committee released their proposed budget reconciliation recommendations in September as part of the Build Back Better Act. The tax legislation would raise $2.9 trillion in revenue to help pay for President Biden’s proposed $3.5 trillion social spending plans. Revenue would be raised primarily by increasing taxes on corporations, and individuals with income over $400k.

While the proposed tax legislation is a draft, it provides us with a look into potential upcoming tax changes. Not only will taxes increase for those earning more than $400k starting next year, changes to the capital gains rates may come as soon as this year. Furthermore, “back door” Roth contributions would no longer be allowed for any taxpayers regardless of income level.

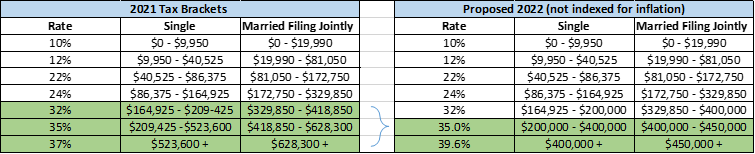

Individual Tax Rates

Those currently in the 32% through 37% tax brackets would see a tax increase on income above $200k for singles and $400k for married filing jointly. The top marginal rate would also apply to estates and trust with income over $12,500. The effective date would apply to tax years starting after December 31, 2021.

Taxpayers that have a Modified Adjusted Gross Income (MAGI) over $5 million will be subject to a new 3% surtax. Because it is based on MAGI, any below-the-line deductions such as charitable gifts, will not reduce the surtax. The surtax would also apply to trusts with $100,000 or more in income.

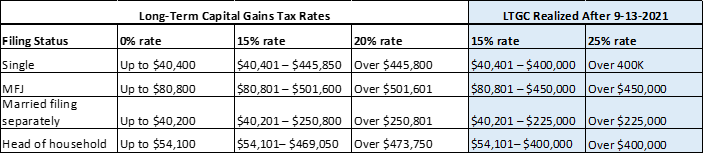

Capital Gains

The top capital gains rate would increase from 20% to 25% for those earning more than $400k annually. Unlike change to the ordinary tax rates, the effective date of this change would apply to gains realized after September 13, 2021.

There is a safe harbor for any recognized gains after September 13, 2021 that occur pursuant to a written binding contract entered into on or before that date[1]. The recognized gains would still be taxed at the lower 20% capital gains rate.

No More Back Door Roth Contributions

Starting in 2022, after-tax contributions made to IRAs or qualified workplace retirement plans can no longer be converted to Roth. This eliminates both the back-door Roth and mega-back-door Roth strategies. This would be a major blow to those who have been utilizing these strategies to increase their retirement savings.

Roth Conversions Restricted

Starting in 2031, Roth conversions will no longer be allowed for those in the highest tax brackets, $400k Single and $450k MFJ (not indexed for inflation). If Roth conversions are something you’ve been contemplating, it will be pertinent to take advantage while you can!

Estate Planning

The TCJA doubled the estate and gift tax exemption levels. Currently at $11.7 million for individuals and $23.4 million for married peopled. The current exemption level is scheduled to expire on December 31, 2025. The new tax legislation would set the expiration date as December 31, 2021, cutting the exemption amount in half starting in 2022.

The use of Grantor trusts would be limited. They will lose their favorable tax status by pulling the trusts into the decedent’s taxable estate. The decedent would be deemed the owner, and any distribution to a beneficiary would be considered a gift. Any asset sales to a Grantor trust would become taxable.

The changes to Grantor trusts would apply to new trusts, and transfers to trusts, on or after the date of enactment of the legislation.

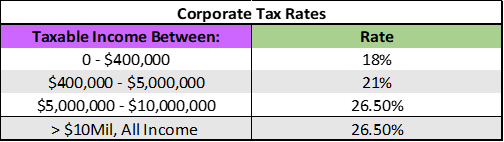

Corporate Tax Rates

The flat corporate income tax of 21% will be replaced with a graduated tax system. Personal services corporations would not be eligible for the graduated rates. Businesses making more than $10 million per year also would not benefit from the graduated tax system. Instead all of their income would be taxed at 26.5%. The effective date is for tax years starting after 12-31-2021.

Net Investment Income

Expands the 3.8% Medicare tax to net investment income derived in the ordinary course of a trade or business. Income, whether from wages, investments, or earnings from a pass-through business, will be subject to the 3.8% tax for single taxpayers with a MAGI over $400k, or $500k if married filing jointly. The 3.8% surtax would not apply to wages on which FICA is already imposed. The effective date is for tax years starting after 12-31-2021.

Limits the Deduction of Qualified Business Income

The maximum allowable pass-through deduction would be limited to $400k for single filers, and $500k for joint filers. There is not a phase-out range based on the amount of income an individual has. The effective date is for tax years starting after 12-31-2021.

What Is Next?

When the tax legislation will go to a vote is yet to be seen. Averting a government shutdown became a priority at the end of September. Progressive Democrats want to pass both the $1T infrastructure bill and the $3.5T social spending bill. Moderate Democrats feel the $3.5T price tag is too big.

Should the tax legislation pass as part of the budget reconciliation this fall, Roth conversions will be an important planning tool in 2021 for those in the top brackets. Completing back door Roth contributions before year’s end will also be pertinent.

Those realizing large capital gains after 9-13-2021 may want to consider deferring those gains to a Qualified Opportunity Zone Fund.

[1] Subtitle I – Responsibly Funding Our Priorities (Source)