Roth 5 Year Waiting Period Rules

10/29/2019By Anne Zavaglia

There are some unclear and misunderstood rules that exist for ROTH IRA distributions.

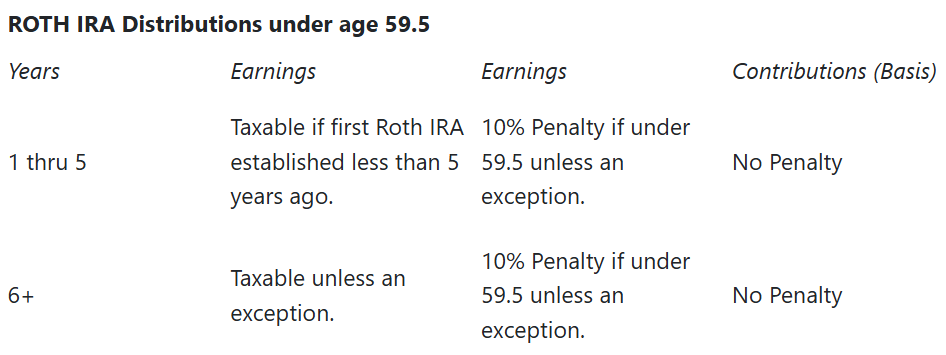

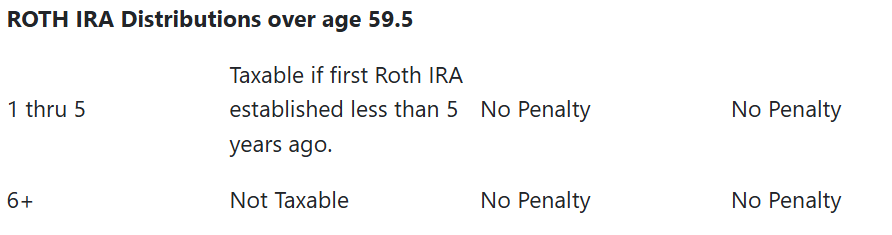

Qualified Distributions, which are both tax and penalty free, are distributions that occur 5 years after the first Roth IRA account is established, and the account holder is over age 59.5. For all other distributions, unless there is an exception, distributions may be subject to penalties and tax.

For earnings to be tax free, an account holder’s first ROTH IRA account must have been established at least 5 years prior to any distributions of earnings. For example, if a person opens their first Roth IRA account at age 56, and takes a distribution at age 60, the earnings will be subject to tax. However, no penalty will apply because they are over age 59.5.

For those under age 59.5, earnings will be subject to a penalty and tax unless there is an exception.

Contributions will not be subject to tax since it is considered a return of basis and was funded with after tax dollars.

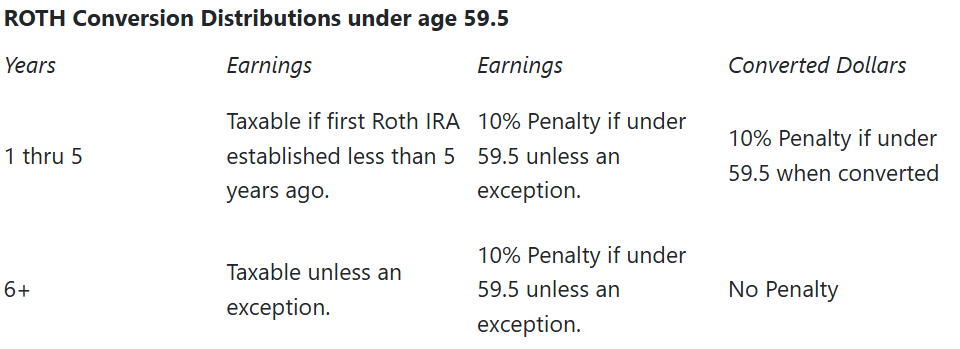

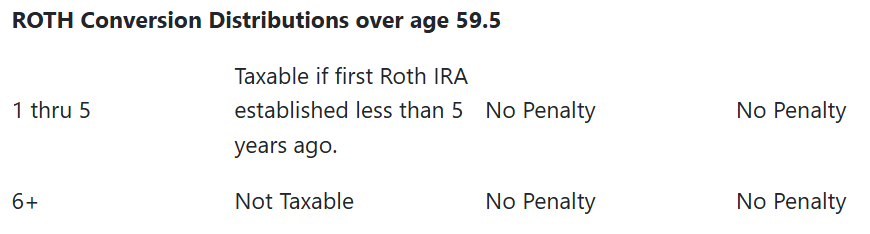

Roth Conversion 5 Year Waiting Period

For those under age 59.5 converting their traditional IRA to Roth, they must wait 5 years after the conversion to avoid penalties on any distributions of converted dollars.

Each conversion, or rollover from a qualified plan, is subject to a separate five-year waiting period.

Those converting traditional IRA dollars after age 59.5 will not be subject to penalties. They may, however, be subject to tax on the earnings if their first ROTH IRA account was established less than 5 years before the distribution.

See the below chart to determine if a distribution is subject to tax or penalties:

*Year one starts on January 1 no matter when during the year the account was opened, or conversion was completed.

**Exception if disabled or $10k for first home purchase.

If you take an early withdrawal from a Roth IRA, contributions come out first, which is a rare move by the IRS to make things easier on you.

You don’t have to worry about taxes — or about accounting for which portion of your distribution comes from earnings, and which from contributions — unless you pull out more than you’ve contributed.

Distribution Order Rules

If you receive a distribution from your Roth IRA that isn’t qualified, you won’t have to worry about taxes or accounting for which portion of your distribution comes from earnings vs. contributions unless you pull out more than you’ve contributed. There is a set order in which contributions (including conversion contributions and rollover contributions from qualified retirement plans) and earnings are distributed from your Roth IRA.

The distribution order:

If you think you will need to take a non-qualified distribution that is more than your total after-tax contributions into the Roth IRA, consult your CPA to calculate any potential taxes and penalties that will be due.

Sources:

nerdwallet

Investment News

irs.gov

There are some unclear and misunderstood rules that exist for ROTH IRA distributions.

Qualified Distributions, which are both tax and penalty free, are distributions that occur 5 years after the first Roth IRA account is established, and the account holder is over age 59.5. For all other distributions, unless there is an exception, distributions may be subject to penalties and tax.

For earnings to be tax free, an account holder’s first ROTH IRA account must have been established at least 5 years prior to any distributions of earnings. For example, if a person opens their first Roth IRA account at age 56, and takes a distribution at age 60, the earnings will be subject to tax. However, no penalty will apply because they are over age 59.5.

For those under age 59.5, earnings will be subject to a penalty and tax unless there is an exception.

Contributions will not be subject to tax since it is considered a return of basis and was funded with after tax dollars.

Roth Conversion 5 Year Waiting Period

For those under age 59.5 converting their traditional IRA to Roth, they must wait 5 years after the conversion to avoid penalties on any distributions of converted dollars.

Each conversion, or rollover from a qualified plan, is subject to a separate five-year waiting period.

Those converting traditional IRA dollars after age 59.5 will not be subject to penalties. They may, however, be subject to tax on the earnings if their first ROTH IRA account was established less than 5 years before the distribution.

See the below chart to determine if a distribution is subject to tax or penalties:

*Year one starts on January 1 no matter when during the year the account was opened, or conversion was completed.

**Exception if disabled or $10k for first home purchase.

If you take an early withdrawal from a Roth IRA, contributions come out first, which is a rare move by the IRS to make things easier on you.

You don’t have to worry about taxes — or about accounting for which portion of your distribution comes from earnings, and which from contributions — unless you pull out more than you’ve contributed.

Distribution Order Rules

If you receive a distribution from your Roth IRA that isn’t qualified, you won’t have to worry about taxes or accounting for which portion of your distribution comes from earnings vs. contributions unless you pull out more than you’ve contributed. There is a set order in which contributions (including conversion contributions and rollover contributions from qualified retirement plans) and earnings are distributed from your Roth IRA.

The distribution order:

- Regular contributions.

- Conversion and rollover contributions, on a first-in, first-out basis (generally, total conversions and rollovers from the earliest year first). Take these conversions and rollover contributions into account as follows:

- Taxable portion (the amount required to be included in gross income because of the conversion or rollover) first, and then the

- Nontaxable portion.

- Earnings on contributions.

If you think you will need to take a non-qualified distribution that is more than your total after-tax contributions into the Roth IRA, consult your CPA to calculate any potential taxes and penalties that will be due.

Sources:

nerdwallet

Investment News

irs.gov