Q2 2026 Market Review

07/06/2026Blog Categories

By Clint Edgington

Our Q1 2026 Market Review focused on how markets responded to the U.S. bombing of Iran. While the direct conflict remained contained, the possibility of a broader regional war caused investors to demand a higher premium for taking risk. That showed up across several markets.

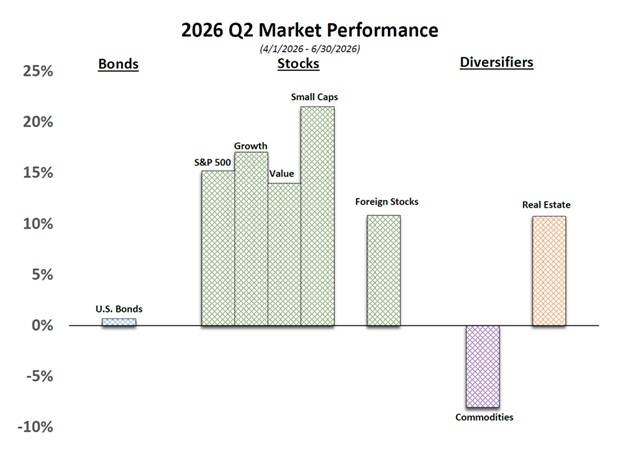

During the second quarter, as various steps were taken to de-escalate the conflict, much of that higher risk premium partially unwound. Commodities gave back much of their first-quarter gains. Growth recovered some of the ground it lost to Value. Risk assets generally outperformed.

Commodities provide the clearest example. Last quarter, markets priced in the possibility of supply disruptions and a broader regional conflict. As those concerns eased, much of that premium came back out of commodity prices.

Growth versus Value was more complicated.

In our Q1 review, we pointed out that Value had already begun outperforming Growth before the bombing of Iran. That raised a broader question: Did the conflict simply accelerate an existing trend, or were we beginning to see a more meaningful shift in market leadership?

Three months later, I don't think we have the answer.

Growth recovered against Value during the quarter, but Value remained ahead for the year. By itself, that doesn't tell us much. The more interesting observation came from looking beyond the largest companies.

If investors were broadly rotating away from Growth, I would expect to see Value outperform regardless of company size. Instead, Small-cap Growth significantly outperformed Small-Cap Value during the quarter. Growth leadership extended well beyond the handful of mega-cap AI companies that have dominated returns over the past two years.

That doesn't mean AI stopped leading. It means the market broadened.

Our AI proxy still gained roughly 48% during the April through early June rally compared with about 19% for the Russell 1000 Growth Index. It also declined considerably more during the June correction before participating fully in the rebound. That's consistent with a higher-volatility segment of Growth, not necessarily a market leader losing its influence.

To me, that's the more encouraging development. Markets tend to be healthier when gains are supported by a broader group of companies rather than concentrated in only a handful of names.

The bond market told a different story.

Unlike equities, bonds participated much less in Q2's partial unwind. Inflation remained stubborn, economic growth held up, and recession fears continued to fade. By quarter-end, markets had largely abandoned expectations for additional rate cuts.

What caught my attention was the Fed's communication.

Compare the March 2026 FOMC Statement with the June 2026 FOMC Statement. The June statement was noticeably shorter and removed much of the forward-looking language investors had become accustomed to.

Chairman Kevin Warsh addressed the change directly during his June 2026 FOMC Press Conference:

"Absent, also, is so-called forward guidance—which we agreed was not well suited to the current policy conjuncture."

The June 2026 Summary of Economic Projections also became more hawkish. In March, no participant projected a federal funds rate above 4% in 2026. By June, six did.

I don't know whether those communication changes explain the bond market's caution. I do think they're worth watching. If the Fed intends to provide fewer clues about where policy is headed, markets will have to place greater weight on incoming data and less on Fed guidance. That's a meaningful change, whether or not it proves to be a lasting one.

Our Q1 2026 Market Review focused on how markets responded to the U.S. bombing of Iran. While the direct conflict remained contained, the possibility of a broader regional war caused investors to demand a higher premium for taking risk. That showed up across several markets.

During the second quarter, as various steps were taken to de-escalate the conflict, much of that higher risk premium partially unwound. Commodities gave back much of their first-quarter gains. Growth recovered some of the ground it lost to Value. Risk assets generally outperformed.

Commodities provide the clearest example. Last quarter, markets priced in the possibility of supply disruptions and a broader regional conflict. As those concerns eased, much of that premium came back out of commodity prices.

Growth versus Value was more complicated.

In our Q1 review, we pointed out that Value had already begun outperforming Growth before the bombing of Iran. That raised a broader question: Did the conflict simply accelerate an existing trend, or were we beginning to see a more meaningful shift in market leadership?

Three months later, I don't think we have the answer.

Growth recovered against Value during the quarter, but Value remained ahead for the year. By itself, that doesn't tell us much. The more interesting observation came from looking beyond the largest companies.

If investors were broadly rotating away from Growth, I would expect to see Value outperform regardless of company size. Instead, Small-cap Growth significantly outperformed Small-Cap Value during the quarter. Growth leadership extended well beyond the handful of mega-cap AI companies that have dominated returns over the past two years.

That doesn't mean AI stopped leading. It means the market broadened.

Our AI proxy still gained roughly 48% during the April through early June rally compared with about 19% for the Russell 1000 Growth Index. It also declined considerably more during the June correction before participating fully in the rebound. That's consistent with a higher-volatility segment of Growth, not necessarily a market leader losing its influence.

To me, that's the more encouraging development. Markets tend to be healthier when gains are supported by a broader group of companies rather than concentrated in only a handful of names.

The bond market told a different story.

Unlike equities, bonds participated much less in Q2's partial unwind. Inflation remained stubborn, economic growth held up, and recession fears continued to fade. By quarter-end, markets had largely abandoned expectations for additional rate cuts.

What caught my attention was the Fed's communication.

Compare the March 2026 FOMC Statement with the June 2026 FOMC Statement. The June statement was noticeably shorter and removed much of the forward-looking language investors had become accustomed to.

Chairman Kevin Warsh addressed the change directly during his June 2026 FOMC Press Conference:

"Absent, also, is so-called forward guidance—which we agreed was not well suited to the current policy conjuncture."

The June 2026 Summary of Economic Projections also became more hawkish. In March, no participant projected a federal funds rate above 4% in 2026. By June, six did.

I don't know whether those communication changes explain the bond market's caution. I do think they're worth watching. If the Fed intends to provide fewer clues about where policy is headed, markets will have to place greater weight on incoming data and less on Fed guidance. That's a meaningful change, whether or not it proves to be a lasting one.