DOL Attempts to change who must act as a Fiduciary

By Clint EdgingtonPosted on September 2nd, 2015

Executive Summary

The Department of Labor has proposed an amendment to redefine and expand who must act as fiduciaries in the retirement plan space and those who give advice for Individual Retirement Accounts. A fiduciary has a legal obligation to act in the best interest of their client. Specifically, they must act with the “care, skill, prudence and diligence…that a prudent man acting in a like capacity and familiar with such matters” would. We applaud the DOL, as we believe there is significant confusion in this area.

For our clients, we always act as a fiduciary already. This rule will not affect them significantly. For plan sponsors who do not work with us, we urge you to understand which, if any, of your providers currently act as a fiduciary. You can find this in the fine print of the 408b(2) disclosure your vendor sends to you as well as in your contract.

If you work with a vendor who was not a fiduciary prior to this rule and will become a fiduciary, you will be liable for any breaches by your co-fiduciary that you knew or should have known about. For example, if you work on a bundled platform (e.g. Schwab or Fidelity) and they don’t take fiduciary liability but provide a system for your participants that will give a recommendation with specific funds, they will become fiduciaries. You will become liable for their actions as a co-fiduciary.

We suspect the Obama administration is pushing the DOL to implement this rule under the current administration and, although the DOL states they will review the comments and make changes, we do not believe they will have time to materially adjust the rule. Therefore, we anticipate it will pass substantially in its current form.

Background

Functionally, we see every day that employers running 401k plans are understandably confused by who is acting as a fiduciary. The people we meet with who are running the 401k plans are intelligent businessmen and women. They are CFOs, HR directors and company owners. However, they generally have no clue who is required to act in their best interests and who isn’t.

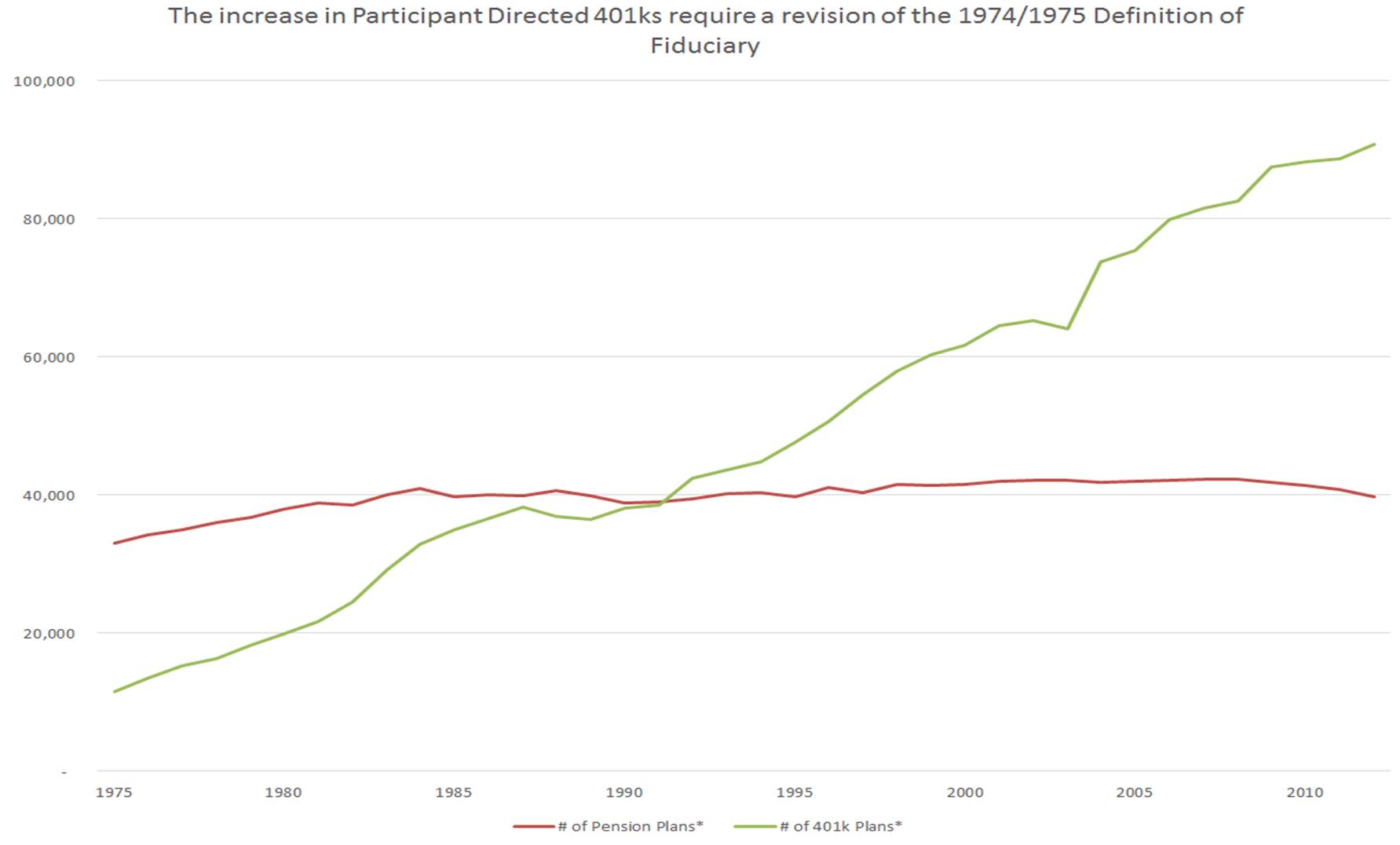

The definition and restrictions of who acts as a fiduciary were implemented in 1974 and 1975. At that time, most retirement plans were professionally managed and defined benefit plans, 401k plans didn’t exist and the IRA market was minuscule¹.

If these advisers are not fiduciaries, they may operate with conflicts of interest that they need not disclose and have limited liability under federal pension law for any harms resulting from the advice they provide. Non-fiduciaries may give imprudent and disloyal advice; steer plans and IRA owners to investments based on their own rather than their customers financial interests; and act on conflicts of interest in ways that would be prohibited if the same persons were fiduciaries.

In light of the breadth and intent of ERISA and the Code’s statutory definition, the growth of participant-directed investment arrangements and IRAs, and the need for plans and IRA owners to seek out and rely on sophisticated financial advisers to make critical investment decisions in an increasingly complex financial marketplace, the Department believes it is appropriate to revisit its 1975 definition.[2]

What Is a Fiduciary?

Any party who renders investment advice for a fee is a fiduciary. Under this new ruling, previous restrictions will be thrown out and the DOL will consider a person a fiduciary with respect to a plan or IRA if that person gives advice that is:

- Pursuant to an agreement,

- Individualized or for use in making investment decisions for a plan or IRA,

- Provided for a fee or compensation, and

- Within four buckets that contain:

1. Recommendations on acquiring, holding, disposing or exchanging securities or other properties, including distributions from a plan or IRA.

2. Recommendations on managing securities or other property.

3. Appraisals, opinions or other statements on the value of securities or other property.[3]

4. Recommendations of a person to give the plan/IRA advice described above.

This definition differs for many reasons, but the major disparity is that it does not require the advice to be given on a regular basis, which is how we generally see providers duck out of the fiduciary duty in the fine print. In addition, it doesn’t need to be the primary basis for investment decisions to trigger the fiduciary duty.

Another major and very contentious difference is that the DOL is now adding fiduciary requirements for IRAs. IRAs generally aren’t plans subject to ERISA and historically haven’t required a fiduciary. The DOL is back-dooring this, using the tax qualified status of IRAs (they receive tax benefits) to use the IRS code to include IRAs in this regulation. This has a lot of political ramifications that makes for an interesting drama[4] between the SEC, the DOL, and Congress.

Additions to Acting Fiduciaries

The DOL’s proposal will create a fiduciary duty for any broker or insurance agent who solicits rollovers from 401k plans or advising in an IRA account. Many of these providers have a different business practice and will have a hard time adjusting. For example, many insurance agents solicit rollovers that sell variable annuities of dubious quality. Previously, they had significantly less responsibility compared to the fiduciary duty. This will change.

Exemptions

For sake of brevity, we will gloss over this; however, attorneys, accountants and actuaries are exempted merely because they provide assistance in connection with a particular investment transaction, and only if they would recommend specific investments or render valuations opinions.[5]

Exclusions

These include:

- Company employees who aren’t already fiduciaries but who act in an administrative role.

- Investment platform providers who put together a set of investment alternatives according to quantitative criteria. We believe this is a weak point in the regulation. Plan sponsors will remain confused and trust the provider is offering that information as a recommendation. We imagine the platform provider’s marketing materials will not help to clarify that.

- Persons providing investment education to plan participants. This may also be a bit of a slippery slope—keeping plan sponsors confused in the same way as above.

- Providers of financial reports and valuations.

On its face, many of the ways brokers and insurance agents get paid would be considered a prohibited transaction under ERISA. To help offset that, the DOL has proposed an exemption to this for a “best interest contract” that would allow them to continue getting paid the same way as long as they comply with requirements to:

- Provide advice according to the client’s best interest.

- Adopt/follow policies to disclose and mitigate conflicts of interest, such as hidden fees paid by investment providers.

We believe it will be fascinating to watch how providers attempt to fulfill this. Specifically, insurance agents who solicit rollovers for annuity sales, or attempt to sell into any IRA will have a tough time fulfilling the first requirement. We see that many of those that are against this plan are attempting to get the DOL to change and soften the duties if they get the “Best Interest” exemption.

There are also carve-outs for certain activities to larger and more sophisticated plans that is beyond the scope of this document.

The Parties

Most consumer protection groups seem to be for it[6]. The CFA Institute has called it “an important step in the right direction,” and we agree. The Financial Planners Association, Consumer Federation of America, and many public pension plans such as CALPERS and the New York State Common Retirement Fund stand for it as well.

Essentially, Wall Street and insurance companies are broadly against it. Generally, their position is that the excess costs will essentially “price out” low- and middle-income population from their services.

The securities and banking industry’s main lobbying organization, SIFMA, has voiced significant opposition[7] as well as most of its constituents. The insurance industry is broadly against it[8] too. And while the SEC believes this should be under its purview, Chairwoman Mary Jo White has stated there should be a uniform fiduciary duty for broker dealers and registered investment advisors. Nevertheless, her ability to win the required support of the majority of the five-member commission seems questionable.

Probable Outcome

We believe the heart of what will be attacked—and the area where the DOL may weaken—is the requirements for the best interest exemption and the duties that those that rely on it will have to adhere to.

However, it seems the Obama administration is intent on getting something passed on this. While the DOL has stated they will take comments seriously and adjust the final rule, it appears unlikely they will have the time to do this and, as previously stated, we believe it will pass largely in its current form.

The change will go into effect 60 days after the final rule is published in the Federal Register and most requirements will become applicable eight months after publication.

What Plan Sponsors need to Do

Sponsors should determine if their service providers are taking any fiduciary liability currently, and in what capacity. If not, they should decide if they will become a fiduciary and understand how that may change things. Also, if they will become a fiduciary, you (as a fiduciary as well) will now be liable for any breaches of a co-fiduciary that you know or should know about.

If your provider submitted a comment letter to the DOL about this change, we recommend reviewing it and seeing if you believe the provider is, in fact, looking out for your best interest.

Please contact us for a complementary review to determine who has the legal duty to act as your fiduciary.

About the Author:

Beacon Hill Investment Advisory provides Fiduciary Advisory solutions to ERISA based retirement plans. We are independent of any platform or investment providers.

Clint Edgington, CFA lives in Grandview with his wife Jenny and sons; Cole, Grant and Connor.

Clint Edgington, CFA lives in Grandview with his wife Jenny and sons; Cole, Grant and Connor.

Mr. Edgington has acted in a fiduciary role for the past decade as a Trustee and also as an Investment Advisor. He has been admitted and testified as an expert witness before the New York Stock Exchange and the Financial Industry Regulatory Authority on his analyses of ERISA based portfolios. Mr. Edgington is frequently published or quoted; including in such publications as; Plan Sponsor Magazine, The Chicago Tribune and The Columbus Dispatch. Clint is a graduate of Miami University and an active member of the CFA Society of Columbus.

[1] Graph: Data source: U.S. Dept of Labor, Private Pension Plan Bulletin Historical Tables and Graphs, Dec. 2014 pg. 5. *Technically Defined Benefit Plans and Defined Contribution plans

[2] Federal Register Volume 80, Number 75, pages 21928 & 21929

[3] While we have condensed a lot of the information that is salient, this particular section has significant carve-outs and exemptions.

[4] SEC Commissioner Daniel Gallagher July 21, 2015, letter to DOL: “It is clear to me that the DOL rulemaking is a fait accompli and that the comment process is merely perfunctory … I was not included in any of these conversations. From a distance—a place where a presidentially appointed SEC Commissions should not be in this context.”

[5][4] Federal Register Volume 80, Number 75, page 21950

[6] http://www.pionline.com/article/20150420/PRINT/304209982/dols-proposed-fiduciary-rule-on-advice-gets-a-thumbs-up

[7]http://www.sifma.org/newsroom/2015/sifma_submits_comments_on_department_of_labor_s_proposed_retirement_regulation/

[8] http://www.dol.gov/ebsa/pdf/1210-AB32-2-WrittenTestimony25.pdf