Will interest rates rise this year?

By Mark FisselPosted on October 2nd, 2013

The Fed hasn’t yet raised its target interest rate from less than 0.25%, and it has promised not to do so before unemployment reaches roughly 6.5%, which it doesn’t expect to happen until next year. However, some interest rates have already begun to go up. For example, according to Freddie Mac, the average interest rate on a 30-year fixed-rate mortgage shot above 4% last June for the first time since late 2011, hitting its highest level in almost 2 years. In the same month, the yield on the 10-year Treasury bond went above 2.5% for the first time since August 2011.

Why are interest rates rising even though the Fed’s target rate hasn’t? Because bond investors are concerned that higher interest rates in the future will hurt the value of bonds that pay today’s lower rates. Immediately after the Fed’s June announcement, investors began pulling money out of bond mutual funds in droves, reversing a multiyear trend. If there’s less demand for bonds, yields have to rise to attract investors.

Aside from bonds, why are investors concerned about a possible Fed rate hike? Bonds aren’t the only financial asset that can be affected by potential future interest rate changes. Dividend-paying stocks with hefty yields have benefitted in recent years; more competitive bond yields could start to reverse that dynamic. Shares of preferred stock typically behave much like those of bonds, since their dividend payments also are fixed; their values could be affected as well.

Also, higher mortgage rates could potentially slow the housing market recovery, though historically they remain at relatively low levels. And if a Fed rate increase were to bring on higher interest rates abroad, that could create even more problems in countries already struggling with sovereign debt–problems that have provoked global market volatility in the past.

The Fed has said any hikes in its target rate will occur only if the economy seems strong enough. If higher rates seem likely to halt the recovery, the Fed could postpone a rate hike even longer. It also will take other measures before raising rates. Even though the timing and size of any Fed action is uncertain, it’s best to be aware of its potential impact.

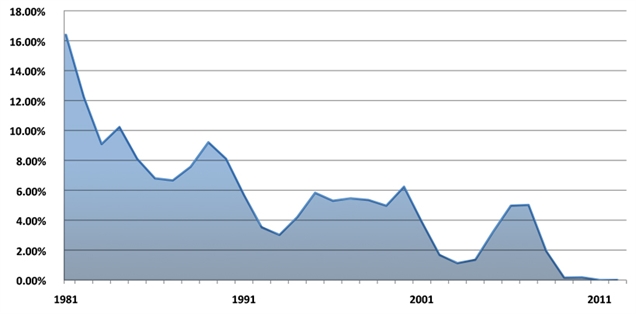

Graph: Interest Rates 1981-2012

This graph represents the federal funds effective interest rate (the average rate at which banks lend to one another overnight), which has generally declined to historic lows over the 30-year period represented. Investment returns, as well as interest rates on bank loans and other fixed-income instruments, could potentially be affected when this rate rises.

Source: Board of Governors of the Federal Reserve System (www.federalreserve.gov), July 17, 2013. Broadridge